Your Life On Paper (What is The Co-operative/Co-op Board Application)

Your Life On Paper

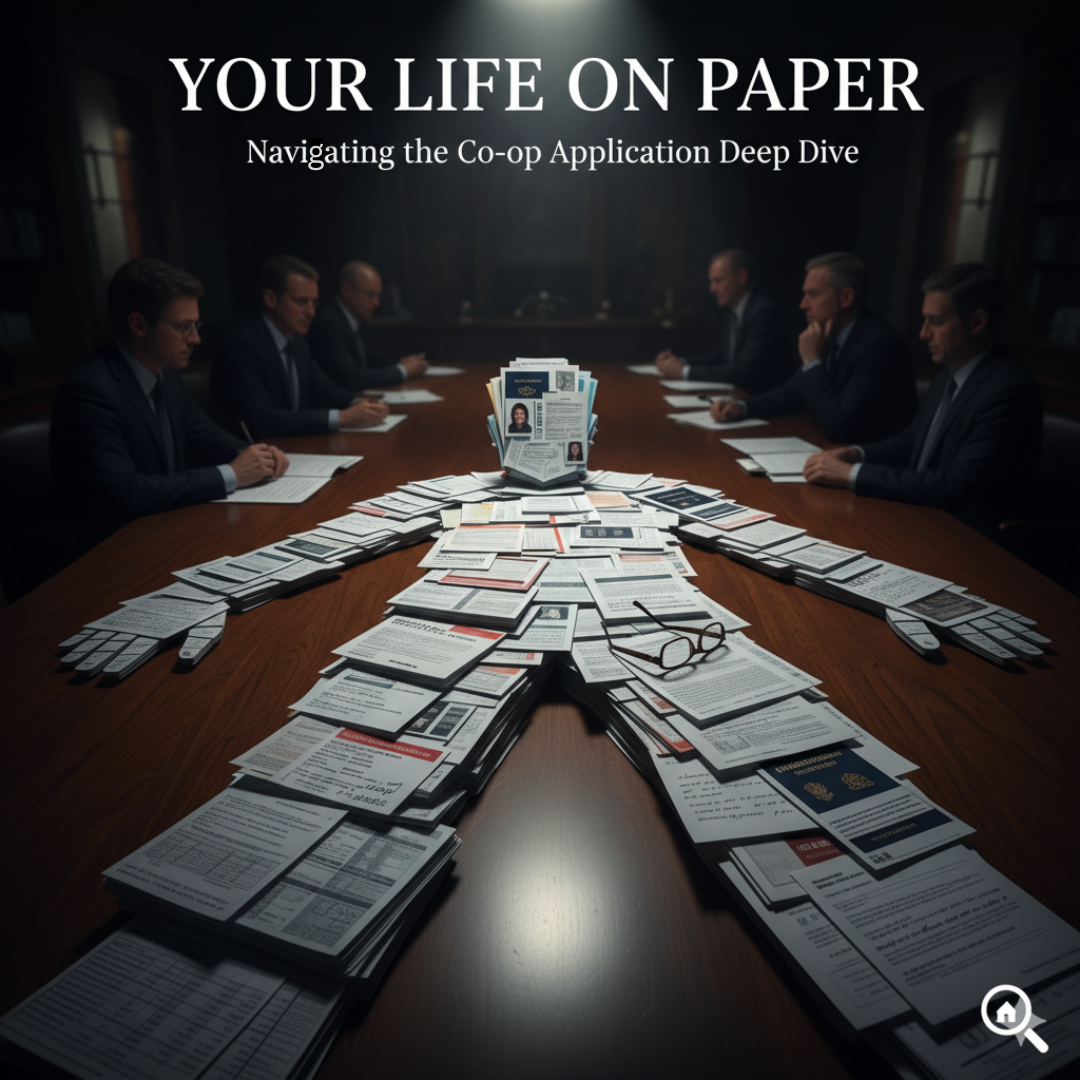

When I work with clients, one of the first things I tell them is that buying a co-op is unlike any other real estate purchase. It’s not just about the numbers or the space; it’s about a deeply personal journey where you quite literally lay your life out on paper for a cooperative board to evaluate. This is why I call the application process, “Your Life On Paper.”

My coaching sessions are focused on preparing you for this experience, and frankly, my success rate—my applicant pass rate—is one of the things I am most proud of. It comes from understanding exactly what the board is looking for and making sure your submission is pristine, complete, and compelling (aka. Boring. Ask me for more info on that.).

The Board Wants to Know Everything

The sheer volume of documentation required for a co-op application can be staggering. You are giving the co-op board a comprehensive, documented look at your past and present life. The application package I review with my clients requires detailed information spanning several key areas:

Financial Health: You must provide tax returns, often for the past three years, along with proof of all bank and investment accounts, sometimes covering the past three months. This includes information on all outstanding debt, liabilities, and assets.

Credit and Background: The board will have access to your credit history and will conduct a criminal background check. They need assurance that you are financially responsible and will be a good fiduciary steward of the cooperative.

Purchase History: Documentation of the purchase of your current home is often required.

Personal and Professional Ties: You must provide extensive references—often one professional, two personal, and one or two financial. This gives them a view of your key relationships, your stability, and your character as seen by others. You may also need to list your recreational interests, club memberships, and affiliations.

Signed Commitments: The application includes signing multiple affidavits and agreements. You will sign an affidavit concerning your financial health, sign waivers, and formally commit to honoring the building's House Rules. Furthermore, you must commit to full disclosure regarding any current or future renovation plans.

In essence, before the board ever meets you, they have compiled a full documented version of your life.

Why So Much Detail?

The reason for this intense scrutiny is rooted in the fiduciary duty of the co-op board. A co-op is a legal corporation, and purchasing a unit means buying shares in that corporation. They need to ensure every shareholder is financially stable, responsible, and committed to the community.

Think of the application as the board’s best tool for an objective decision. They review the facts and figures—the credit scores, the tax returns, the bank statements—to determine if you meet their financial and behavioral standards. Only after they have reviewed and approved your comprehensive application will they typically call for an in-person interview.

The interview serves as a final verification that you are, in fact, the person represented in the documents. By making the initial decision based strictly on the paperwork, the board establishes a clear, documented, and defensible rationale for their decision, long before they ever see you face-to-face.

Mastering this process is key to a smooth closing. If you’re preparing to enter the co-op market, I’m here to guide you every step of the way to make sure your Life On Paper is perfectly presented.